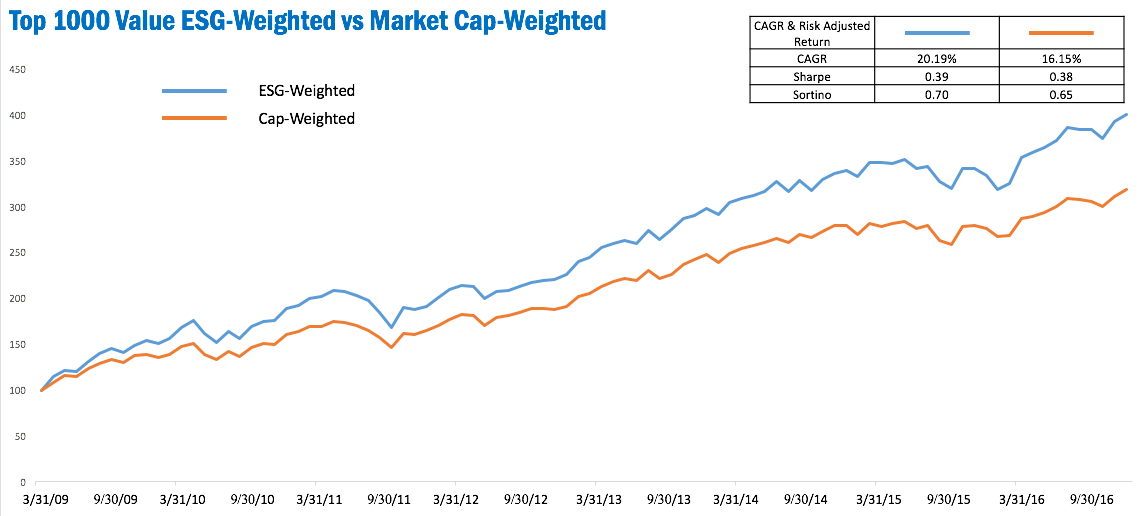

Among our many tests, we made an effort to test our methodology on approximations of popular benchmark indices. This study simulates an ESG-weighted Top 1000 Value portfolio (blue) versus the same portfolio weighted by market-cap (red). Our starting universe is the top 1000 US companies by market-cap that are also in the Wilshire Large- or Mid-Cap Value indices.

Once again, the ESG-weighted portfolio takes an early lead and keeps climbing. Compared to our second study, the ESG-weighted portfolio shows less increase of risk over its cap-weighted benchmark. Like earlier studies, the ESG-weighted portfolio shows low added risk measured by the Sharpe ratio, but higher upside volatility gauged by the Sortino ratio.

We’re liking the way these ESG-weighted portfolios are looking. Drop us a line and let us know what you think.

Disclosure: March 31, 2009 is the date that the OWL ESG historical database begins. The top 1000 US companies are not all covered in the OWL ESG database. Any companies not covered received a weight of 0.00% and their performance is not reflected in the OWL ESG-weighted simulated portfolio. Both portfolios for which the performance is displayed are simulated portfolios; they are non-investible models; there are no investible products tracking them; performance is based on simulated backtests. Factor exposures other than ESG score, such as market capitalization, valuation ratios, and momentum have an effect on performance as well. Past performance is in no way indicative of future results.