How focusing on Scope 1 and 2 emissions in the quest for better low-carbon products can create a real and meaningful pathway to net-zero.

Fueled by a new generation of investors for whom ESG concerns are top priority, the number of investment products with a focus on sustainability is growing fast and the magnitude of capital inflows to these funds suggests the trend is accelerating.

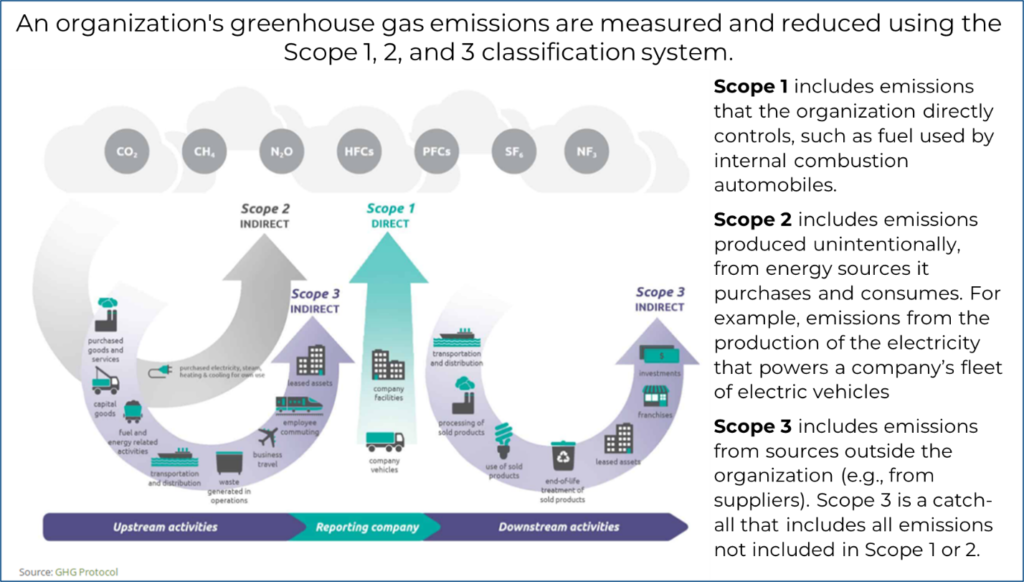

But what exactly is a low-carbon investment product? The question is not as simple as it first appears, due in large part to the wide variety of ways carbon emission reduction can be measured. There are three general categories of emissions – Scope 1, 2, and 3.

Initially, businesses concentrated on lowering Scope 1 and 2 emissions, as these are under their direct control. They achieved this by using less carbon-intensive energy sources, enhancing windows and insulation, and modernizing emission-reducing machinery, among other sustainability-focused practices.

More recently, in response to market demand – driven by several high-profile campaigns focused on Scope 3 – businesses are increasingly giving this class of emissions even higher priority.

Of course, when done cost-effectively, reducing emissions at any level of a company’s activities can be advantageous. It can boost earnings and reputation, while delivering a real and measurable environmental impact.

Scope 3 emissions have the drawback of being difficult to measure, relying heavily on modeling and estimation. Results are notoriously sensitive to a company’s selection of supply chain metrics. Even seemingly insignificant tweaks can have a big impact on the bottom line.

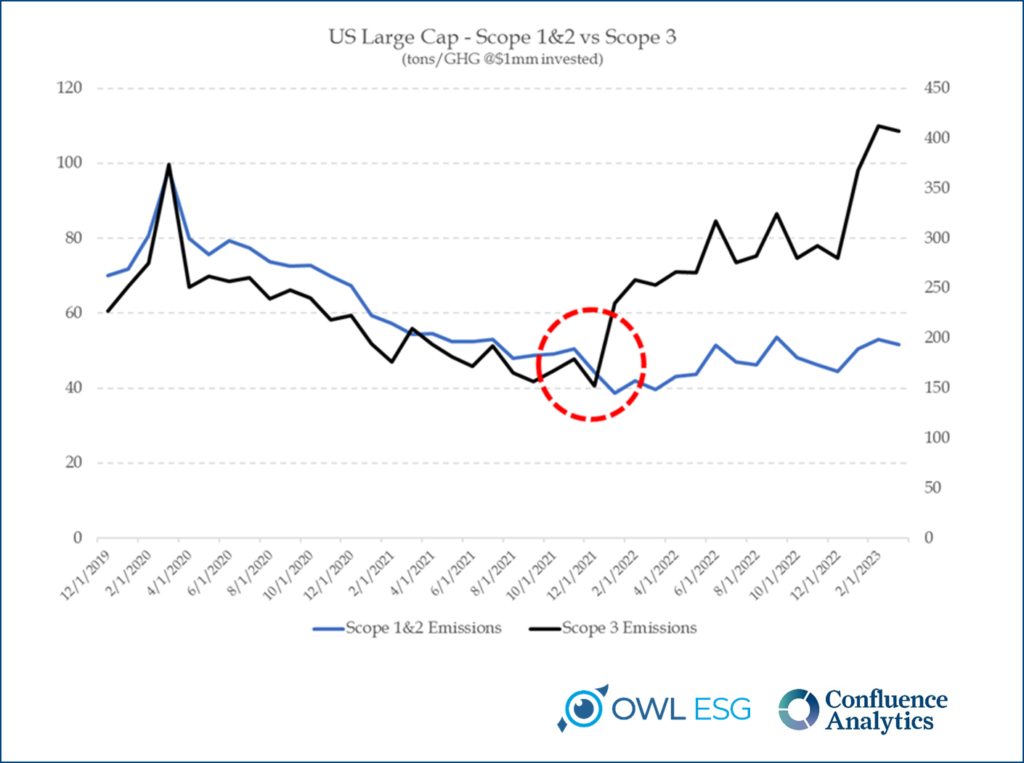

As we can see in the graphic below, Scope 1 and Scope 2 emissions have been declining steadily. Meanwhile, Scope 3 emissions appear to have bounced and are re-gaining intensity as of January 2022. However, what this chart actually demonstrates is how unreliable Scope 3 measurements are as a benchmark for reducing GHG emissions.

In January 2022, major GHG data vendors changed their models, but they did not backfill the changes. The bounce has nothing to do with an increase, or decrease, per se, in actual GHG emissions overall, but simply reflects a change in inputs and expanded ambit of what is counted and reported as Scope 3 emissions, as models were updated to reflect additional disclosures.

Businesses are answering the call to minimize overall emissions; if investors continue to prioritize the measurement and reduction of Scope 3 emissions, companies will almost certainly follow suit. However, this would require resources to track emissions and reductions, not to mention cooperation from suppliers. It’s not clear whether such an expensive strategy would be practical, nor that it would lead to a better overall result in pursuit of reducing GHG emissions.

The Scope 1 and Scope 2 emissions of a company’s suppliers are typically already included in its Scope 3 emission totals, as 100 percent of a company’s Scope 3 emissions are Scope 1 or 2 emissions for another entity. Depending on the size of the supply chain, as well as the intricacy of the operational linkages, GHGs can be grossly overcounted.

Instead, if investors push portfolio companies to focus on reducing Scope 1 and 2 emissions, this would address excessive GHG emissions at their source.

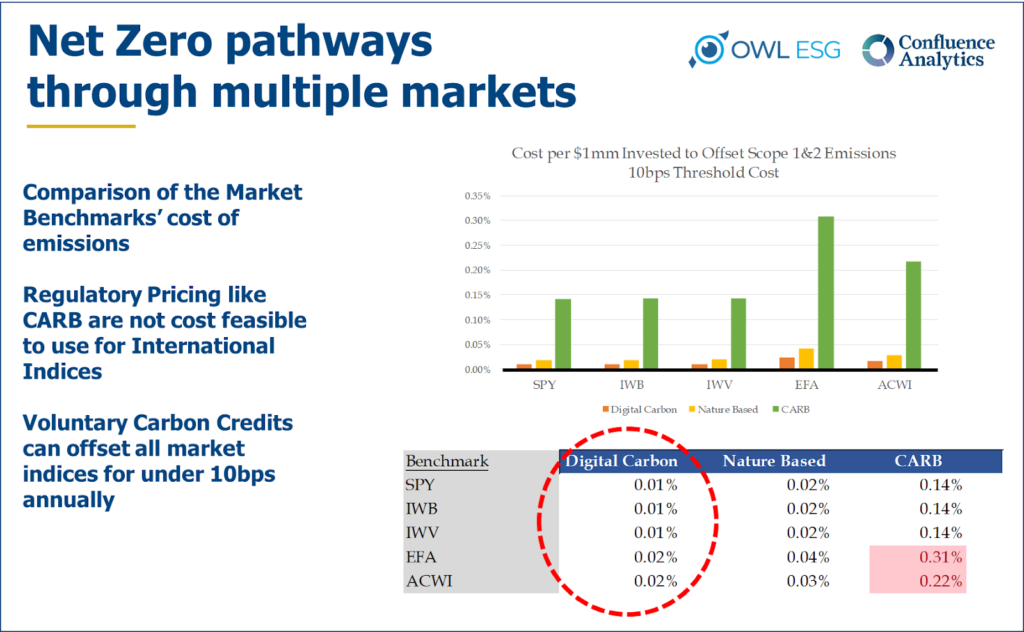

Reducing Scope 1 and 2 emissions, of course, requires pricing Scope 1 and 2 emissions. Fortunately, there are tools available to efficiently price Scope 1 and Scope 2 emissions, and there are also investment options that concentrate on lowering these pollutants, all in pursuit of a truly net-zero market.

For example, Confluence Analytics‘ pricing approach, leveraging emissions as a factor in portfolio construction, provides a more direct – and profitable – route to net zero investing. Confluence has developed a series of ESG signals centered around looking for relationships in residual returns with changes in ESG and carbon data.

When you explicitly include the cost of carbon as another factor to optimize versus risk it makes a profound impact on portfolio composition and outcomes versus the benchmark. The result is a more efficient portfolio in both terms of overall market risk and carbon costs versus a standard index.

This type of optimization can also be useful in intra-sector stock selection, and long- / short- portfolios, which we will explore in detail in a subsequent article.

The basic idea driving this is an old, tried-and-tested as true market perspective. Fundamentally, marrying stock equity risk with cost creates more aligned outcomes for both traditional and sustainability-focused investors.

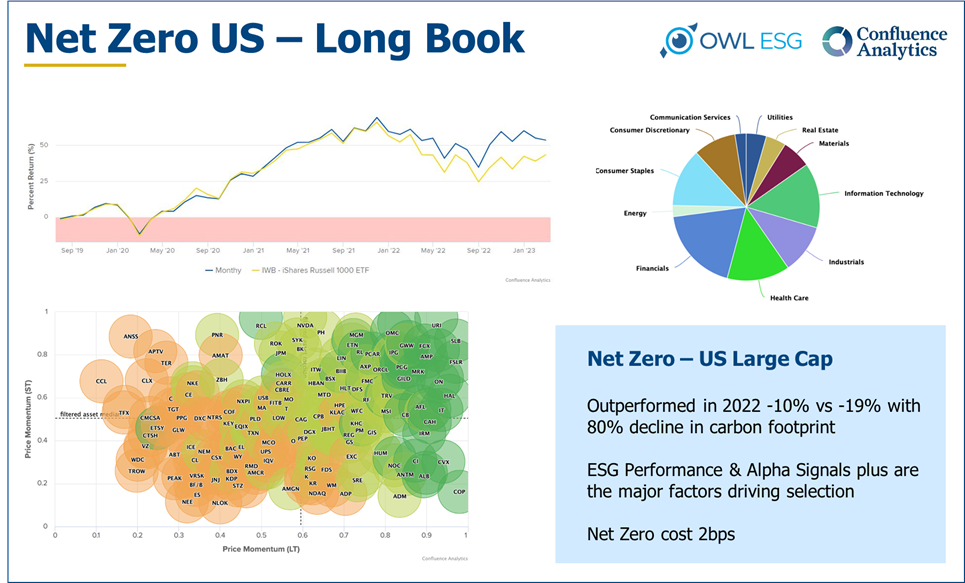

As reflected in the graphic below, tying equity risk with cost would’ve resulted in an 80-percent reduction in carbon footprint with more than 500bps of outperformance in 2022. Under this model, the remaining emissions are systematically offset quarterly.

Of course, there are always potential complications. Previous attempts at market-based carbon offsets have been fraught with accusations of poor quality. In other words, without a robust process that effectively verifies the actual reduction in emissions promised with an offset, bad faith actors could take advantage of trust-based offset product marketing.

This concern has been almost completely alleviated in recent years, as technological developments, including applications of blockchain verification and satellite overlays built into comprehensive reviews, help ensure that carbon offsets are actually doing what they claim.

This is not free, though, and further challenges to carbon offsets and pricing center on the perceived audacity of adding any additional cost to the investment process. More effective than trying to control investment practices in reducing cost is finding a standard around which pricing can be efficiently incorporated into market forces.

Ultimately, meaningful emissions reduction will never happen without a market that financially incentives reducing emissions. To reduce emissions requires measurements that are accurate, clear, and widely accepted. Scope 3 emissions fail to meet any of these tests.

Further, incentivizing market forces to reduce emissions requires that emissions can be priced, with cost tied to risk, and that the pricing drives positive returns. As demonstrated above, this is not only possible, but there are models available that achieve all of these specifications, focusing on Scope 1 and Scope 2 emissions.

Resource expenditure on vaguely defined and difficult-to-control Scope 3 emissions is arguably counterproductive when that time and money could be dedicated to implementing effective strategies that work toward net-zero by addressing Scope 1 and Scope 2 emissions.