BY: Robert Yates & Barry Greenblatt

In this paper, we present the case that thoughtful ESG Risk Assessment Policies and Procedures are a critical component of underwriting and investment decisions. With proper execution these Policies and Procedures will lead to higher and more stable results for capital providers. This is the first of a three-part series exploring ESG and its role in strategic considerations for capital providers.

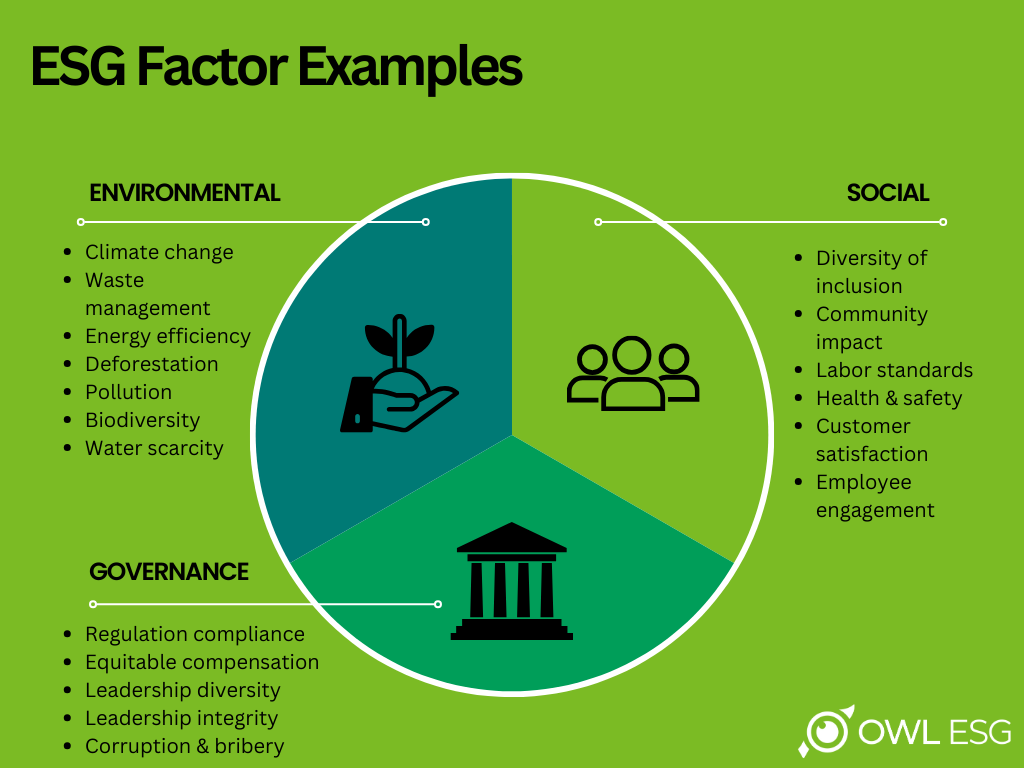

Environmental, Social, and Governance, or “ESG,” is an umbrella term for all environmental, social and governance considerations incorporated in the operational and strategic activities of a corporation or institution. While the term is popular, its meaning can vary from situation to situation. It encompasses a huge range of topics, including climate change/environmental impacts, diversity and inclusion, labor/pay practices, and supply chain issues. The diversity of potential issues that fall under the “ESG Banner” can overwhelm firms and individuals trying to incorporate ESG risks into analysis and decision making when providing capital/credit. In particular, entities that provide capital face challenges in understanding where ESG fits into their lending and investing decisions. Moreover, stakeholders of these capital providers (equity owners, investors, depositors, etc.) are expecting affiliated capital providers to have well-reasoned, thoughtful, and consistent applications of ESG Risk into policies and decision-making. More and more, banks, insurance companies, and investment firms are being asked by their respective stakeholders to explain how ESG and ESG risks are accessed in the decision-making process.

Instead of trying to define ESG, for capital providers it is perhaps more effective to ask what ESG is doing, and why it matters, when a firm is providing capital to another entity. First, it is important to put ideology aside. Blanket statements around absolutes tend to be unhelpful and counterproductive. Firms that effectively incorporate ESG into their strategies and operations generally present capital providers with lower-risk and predictable lending opportunities. This is the profile of an acceptable borrower. For example, firms that implement transparent hiring and promotion policies are less likely to suffer from employee litigation and will, generally, attract higher quality employees. Corporate America has recognized this for decades. Strong human resource activities have led to better performance and improved credit profiles at firms where they are prioritized. Further, entities that consider lower fossil fuel usage in their operations are likely to see consistent expense stabilization over time while concurrently appealing to customers who are concerned with the impact that fossil fuels have on climate change. Borrowers focusing on ESG Risks as part of their strategy and operations provide capital providers with more resilient and stable risk profiles. As a result, capital providers ought to make similar consideration of ESG Risk in their assessment.

In our shareholder capitalism system, the goal of a business entity is to maximize returns. Managing ESG issues is a normal progression for firms building accretive value chains with multiple stakeholder groups, including customers, employees, communities where a firm does its business, lenders, and shareholders.

Based on research done on the topic, the evidence increasingly suggests that firms incorporating robust ESG criteriain their strategies and operations are likely to see shareholder value increase while lowering their overall cost of capital. This should not be surprising. A company’s success is dependent on its stakeholders; employee satisfaction aligns with productivity, good community relationships lower transactional costs, positive brand reputation grows and sustains customer bases, and so on. By incorporating ESG factors into business decisions, a company is positioning itself for success in a market that cares increasingly about those factors.

Capital providers should follow suit. Failure to incorporate ESG factors into corporate decision-making can introduce risk, sometimes significant, affecting a firm’s operations and returns. The most prominent example of this is the increasing focus of regulators on company reporting and action. While many robust regulatory regimes exist already, primarily in Europe, many more are coming, especially in the U.S., where the SEC, OCC, and FRB are beginning to require ESG disclosure in prescriptive ways. Regulatory scrutiny for non-compliance can lead to fines, actions, legal trouble, and more.

Further, companies that have not adapted to the broader focus on ESG factors face potential reputational harm and a subsequent loss of customers. Studies have shown that nearly 85 percent of people will choose a brand that operates in a sustainable manner when price is nearly the same, and 55 percent will pay more for a sustainable brand. Additionally, the companies that are adapting now are less likely to suffer negative operational exposures such as water scarcity, labor disputes, supply chain breakdown, or increased insurance costs. These are all relevant factors that capital providers need to consider.

Capital providers have always faced challenges in evaluating the risk of a potential borrower. Markets are volatile, and customer preferences change rapidly. Stable firms can experience swings in customer and investment sentiment at astonishing speeds. Capital providers are beginning to understand that a client’s ESG risk profile is as relevant as traditional areas of assessment such as management and financial stability. ESG is a risk that must be considered, priced, and mitigated.