Sustainable investing and long-term investing share significant overlap. Investors use both approaches to seek specific positive change over broad periods of time. Without financial returns, sustainable investing is futile, and blue-chip, dividend paying stocks are a critical component of many successful long-term investment strategies. These established companies tend to be more carbon-intensive for a number of reasons, seemingly creating conflict between the two investment approaches. But there are ways to include stable, blue-chip companies in a sustainable portfolio, even with some names that might seem counterintuitive, by looking at dividends and the “climate-adjusted yield.”

To compare how effective companies are in implementing their sustainability strategies, such as reducing greenhouse gas (GHG) emissions, we need a standard way to measure the cost of doing business. Establishing a baseline makes it possible, for example, to price carbon in a market setting, confirm the efficacy of carbon offsets, and evaluate decisions in terms of cost (in basis points), and the impact on risk and return from an investor’s perspective.

Once a baseline is established, the market can reliably evaluate a company’s impact, positive and negative, against an expected return on investment. Of course, yield and return are complicated and difficult to predict, even for the most sophisticated institutional investors. Stable (low volatility) stocks that so many investors crave can lose some of their luster when non-financial objectives enter the equation, with a potentially substantial impact on returns. As an extreme example, fossil fuel companies would not deliver the same returns if they stopped selling fossil fuels.

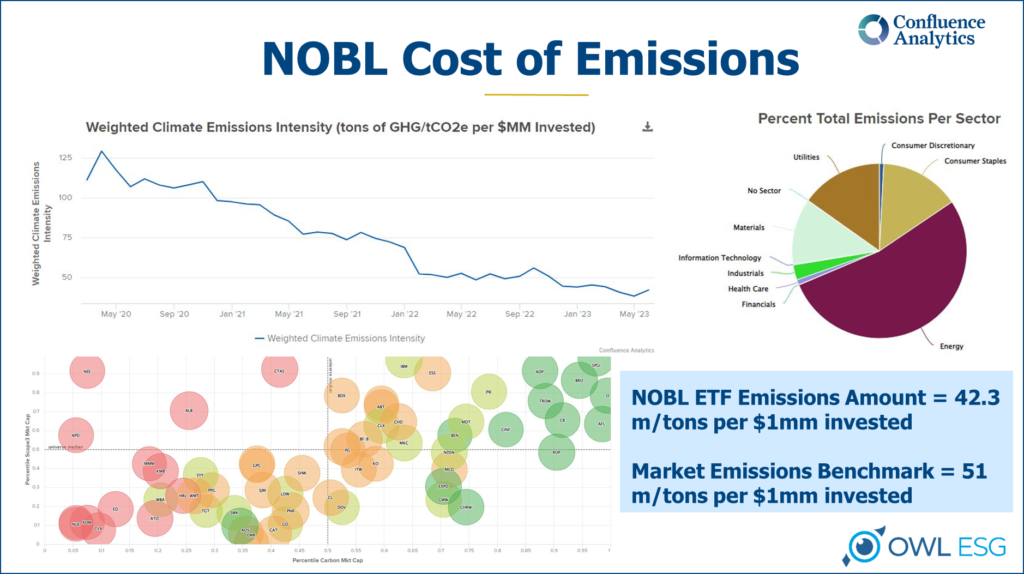

Figure 1 shows the emissions intensity of the ProShares S&P 500 Dividend Aristocrats ETF has declined over time as the composition of this group of high quality dividend payers has shifted.

This concern holds true to an even greater extent for income-oriented investors, who tend to be loyal investors who view their stock positions as long-term relationships, and count on dividend yields to be a substantial component of returns over time. Blue-chip companies with long histories of reliable dividend payments satisfy this criteria perfectly; however, this often creates a conflict for sustainability-focused investors, as these companies are often emissions-intensive, for several reasons. In other words, sustainable investors often appear to be faced with a choice between stable, predictable returns or low-emission companies.

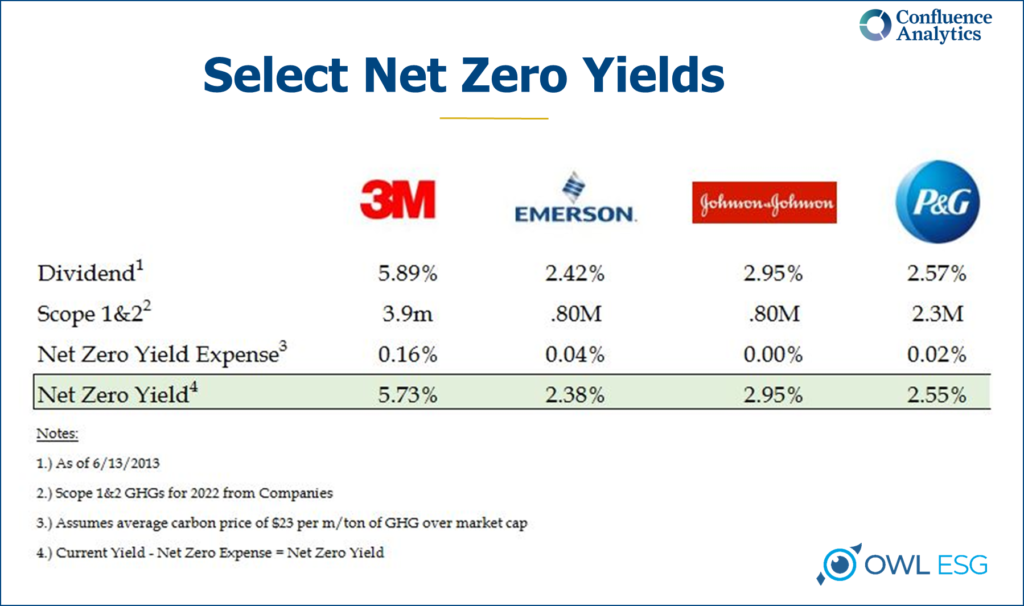

The truth is, this is a false dichotomy. With an established price of carbon, investors can invest their money in the stocks of these respected companies, even those which are not usually associated with being “green.” By multiplying the cost of carbon by total emissions, and then dividing the result by a company’s market value, investors can calculate a straightforward “cost of carbon metric,” expressed in basis points. Subtracting that from the company’s dividend yield produces a “Net Zero Yield,” which we define as the return provided from the company’s dividends adjusted for the cost-of-carbon.

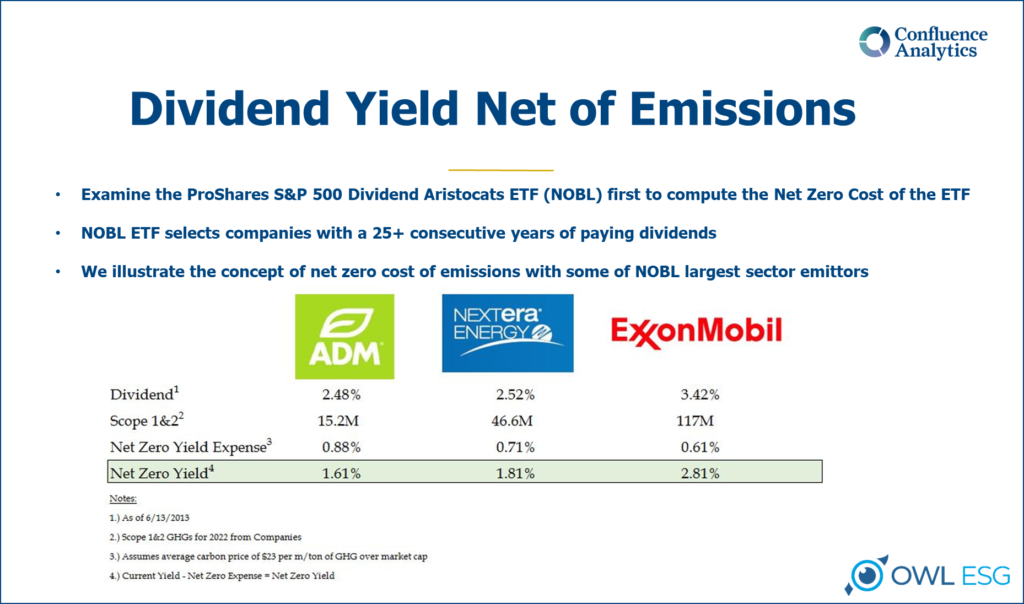

Not only does this approach offer investors a clear way to be both income-oriented and sustainability-minded, it creates a language for companies and investors alike to discuss the cost of—and returns from—taking meaningful steps to reduce carbon intensity through offsets. As Figure 3 shows, viewed through this Dividend Yield Net-of-Emissions lens, companies like ExxonMobil are not only friendly to sustainable investors, they have a powerful market incentive to address carbon-emissions intensity.

In fact, the impact of a sustainable investment dollar is greater at bigger companies with higher market caps, where the cost per ton of offsetting carbon has a fairly small impact on the emissions-adjusted yield. The market has provided a clear way to make investments that are both sustainable and provide stability through dividends. In other words, it is surprisingly easy to have your sustainability cake and eat your financial returns, too. Using this approach, the GHG externality translates into a quantifiable input in the equation used to measure return through yield.

Companies that fail to boost investors’ bottom lines will quickly wither without investment money, regardless of how “green” they might be. For example, evaluating both overall returns and “climate-adjusted yield” as accurately as possible is paramount to a portfolio manager who is seeking to reduce the impact of greenhouse gas (GHG) emissions in a portfolio by selecting companies that are sustainable financially and environmentally. As sustainable investments deliver repeated financial successes, positive change accelerates in non-financial categories, like emissions reduction, with market forces as an engine.

If market forces are the engine of change, yield is the fuel that makes that change meaningful. Yields that are both high and reliable are attractive to nearly all income-oriented investors, regardless of the degree to which they are influenced by sustainability issues. For investors who are also focused on sustainability, the only distinction is that they see yield in terms of return on their investment both in terms of progress toward a greener future, and dollars. In other words, we believe sustainable investing can and should involve the same considerations inherent to any investment strategy, with stocks selected based on expected returns against peers, the overall market, expectations, and a host of other factors.